Social Security Solvency Crisis 2026–2032: CRFB Warnings, Trust Fund Depletion, and the Roadmap to Solutions

The U.S. Social Security Trust Fund is on track to be depleted in just over six years. When that happens, more than 60 million beneficiaries will face an automatic 22% reduction in benefits. Using the latest 2026 data from the CRFB, CBO, and SSA Trustees Report, we break down the reality of the crisis and the realistic solutions lawmakers must consider.

What is the Social Security Solvency Crisis and how can we fix it?

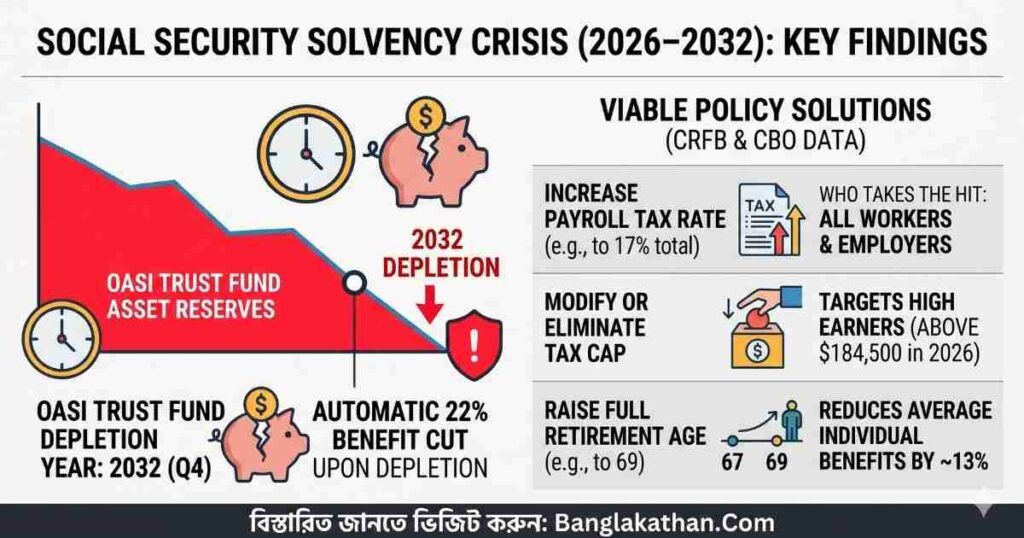

The Social Security Solvency Crisis occurs because the program is paying out more in benefits than it collects in payroll taxes, slowly draining its reserve Trust Fund. According to the 2026 SSA Trustees Report, the Old-Age and Survivors Insurance (OASI) Trust Fund will be depleted by Q4 2032. Once depleted, by law, benefits will be automatically reduced by roughly 22%. Experts suggest the crisis can only be fixed through three paths: (1) Raising revenues (like increasing the payroll tax or cap), (2) Adjusting benefits (like raising the retirement age), or (3) A combination of both. The Committee for a Responsible Federal Budget (CRFB) warns that delaying these reforms will only make the eventual solutions more painful for American workers and retirees.

1. How Does Social Security Actually Work?

Signed into law in 1935, Social Security is the largest federal safety net program in the United States, providing benefits to retired workers, their dependents and survivors, as well as disabled workers.

How is it funded?

Social Security relies almost entirely on two streams of income:

- Payroll Taxes: Workers and employers each pay a 6.2% tax (12.4% total) on earnings. Self-employed individuals pay the full 12.4%.

- Interest Income: Surplus money collected over the decades was deposited into a Trust Fund and invested in special Treasury bonds, generating interest.

Currently, this payroll tax only applies to the first $184,500 of a worker’s earnings (as of 2026). Any income earned above this cap is not subject to Social Security taxes.

Social Security operates via two distinct Trust Funds: OASI (for retirees and survivors) and DI (for disability). The OASI fund is the one facing imminent depletion. The DI fund remains financially healthy through at least the end of the century.

2. The Trust Fund Crisis: What the 2026 Numbers Say

The 2026 SSA Trustees Report

The 2026 Social Security Trustees Report revealed that the Old-Age and Survivors Insurance (OASI) Trust Fund will be entirely depleted by the fourth quarter of 2032. Once the reserves drop to zero, ongoing tax revenue will only be sufficient to cover 78% of scheduled benefits.

This represents a deterioration from previous projections. The timeline moved up by a full year compared to previous reports, largely influenced by recent downward adjustments in fertility and immigration projections, as well as macroeconomic factors.

The timeline was also accelerated due to the “One Big Beautiful Bill Act,” enacted in July 2025, which impacted ongoing federal revenues and tightened the window for the Trust Fund’s survival.

What does this mean for the average American?

If lawmakers fail to act, the Committee for a Responsible Federal Budget (CRFB) estimates that a typical dual-income couple retiring around the time of depletion would face a devastating $18,400 annual reduction in their benefits. For millions of seniors living on fixed incomes, a sudden 22% drop will be economically disastrous.

3. CRFB Warnings: Why Immediate Action is Critical

The Committee for a Responsible Federal Budget (CRFB), a non-partisan, non-profit organization monitoring U.S. fiscal policy, has been aggressively sounding the alarm on the impending insolvency.

Key Findings from CRFB’s Latest Analysis

- The Shortfall is Growing: The 75-year shortfall has grown to approximately $30 trillion.

- Delay Costs More: Reforms that could have easily saved the program twenty years ago—like minor adjustments to the tax cap or indexing—are no longer enough.

- The “Do Nothing” Tax: The CRFB warns that legislative inaction is effectively a vote for a sweeping 22% benefit cut for all retirees.

According to the CRFB and the SSA Chief Actuary, to restore long-term solvency today would require an immediate 4.25 to 4.6 percentage point increase in the payroll tax, a 25% reduction in total benefits, or a mix of both.

4. Crisis Timeline: 2026 to 2034

SSA Trustees release their annual report projecting OASI depletion by Q4 2032. The Penn Wharton Budget Model projects depletion in early 2033. Pressure mounts on Congress.

Trust Fund reserves enter a critical steep decline. If Congress waits until this window to pass reforms, changes will have to be abrupt, likely removing any chance of “grandfathering in” near-retirees to protect them from cuts.

The OASI Trust Fund reaches $0. Under current law, the program can only spend what it brings in, triggering an automatic ~22% reduction in benefits (meaning only 78% of scheduled benefits are payable).

If the OASI and Disability Insurance (DI) funds were legally combined, the combined OASDI fund would deplete in Q3 2034. At that point, 83% of scheduled combined benefits would be payable.

5. Social Security Solvency Solutions: 6 Viable Paths

As SSA Chief Actuary Karen Glenn recently noted, “It’s a simple math problem—it’s not a simple political problem. We need to either raise scheduled revenue, reduce scheduled benefits or some combination of the two”.

Solution 1: Increase the Payroll Tax Rate

The current combined payroll tax is 12.4%. Bumping this up by 4.6 percentage points (to 17% total, or 8.5% for both employers and employees) would close the entire funding gap. However, critics argue a near-20% payroll tax burden would stifle hiring and wage growth.

Solution 2: Modify or Eliminate the Payroll Tax Cap

Currently, earnings above $184,500 are exempt from the Social Security payroll tax. Proposals range from completely eliminating the cap to creating a “donut hole” (where income between $184,500 and $400,000 is exempt, but earnings above $400,000 are taxed). The SSA estimates these strategies would close between 22% and 67% of the funding gap.

Solution 3: Implement an Employer Compensation Tax

A newer proposal from the CRFB involves replacing the employer side of the payroll tax with a flat “Employer Compensation Tax.” This would tax all employer compensation—including wages, stock options, and health benefits—raising an estimated $2.5 trillion over a decade and closing two-thirds of the shortfall.

Solution 4: Raise the Retirement Age

The current full retirement age is 67. The Congressional Budget Office (CBO) found that raising the full retirement age to 69 would shrink annual benefits by roughly 13% per person on average, drastically reducing program costs over time. Opponents argue this disproportionately harms blue-collar workers with lower life expectancies.

Solution 5: The “Six Figure Limit”

The CRFB has proposed establishing a “Six Figure Limit” (SFL) that caps maximum benefits. A couple retiring at the Normal Retirement Age would receive no more than $100,000 annually, and a single retiree no more than $50,000. This targets reductions strictly at the wealthiest retirees.

Solution 6: Adjusting the Benefit Formula

Social Security uses a progressive formula to calculate payouts. By tweaking the “bend points” in this formula, Congress could gradually reduce the benefits paid to high earners while preserving or even enhancing the benefits paid to low-income earners, closing part of the shortfall.

6. Solution Comparison: How Much Does Each Fix?

| Proposed Solution | Impact on Funding Gap | Who Takes the Hit? |

|---|---|---|

| Raise Payroll Tax by 4.6% | Closes 100% of the gap | All workers and employers |

| Eliminate/Modify Tax Cap | Closes 22% – 67% of the gap | High earners (above $184,500) |

| Employer Compensation Tax | Closes ~67% of the gap | Employers |

| Raise Retirement Age to 69 | Reduces outlays (~13% per person) | Future retirees |

| Six Figure Limit ($100k Cap) | Varies by index scaling | High-income retirees |

Source Data: CRFB, CBO, SSA Actuarial Estimates (2026)

7. Why Hasn’t Congress Fixed It Yet?

If the math is simple, why the delay? The answer lies in political calculus.

- Partisan Gridlock: Generally speaking, Republicans oppose major tax hikes, preferring benefit or age adjustments. Democrats oppose benefit cuts or raising the retirement age, preferring to increase taxes on the wealthy.

- The “Third Rail” of Politics: Social Security is incredibly popular. Politicians fear that voting to cut benefits or raise taxes will cost them re-election.

- Lack of Immediacy: Because the absolute depletion date is still six years away, lawmakers tend to prioritize issues that affect the current budget cycle rather than tackling a long-term structural deficit.

The last major, successful overhaul of Social Security occurred in 1983. Faced with a Trust Fund that was mere months away from depletion, President Ronald Reagan and Speaker Tip O’Neill brokered a bipartisan compromise that raised the retirement age and increased payroll taxes. Experts agree a similar bipartisan grand bargain is the only way forward today.

People Also Ask

🔍 Common Questions About the Crisis

- ▶ Is Social Security going bankrupt? — No. “Bankrupt” implies it will hit zero and stop paying entirely. Even after the Trust Fund depletes in 2032, ongoing tax revenues will cover 78% of scheduled benefits.

- ▶ What does Social Security Solvency actually mean? — Solvency refers to the Trust Fund’s ability to pay 100% of promised benefits. Insolvency means the reserve is gone, forcing the system to rely strictly on real-time tax income.

- ▶ How credible is the CRFB? — The Committee for a Responsible Federal Budget is a highly respected, non-partisan organization. Their numbers align closely with the Congressional Budget Office (CBO) and the SSA’s Office of the Chief Actuary.

- ▶ Will current retirees see a cut? — Yes. If Congress allows the Trust Fund to deplete, the automatic 22% cut will apply to all beneficiaries—both future and current retirees.

Detailed FAQs

📚 References & Source Data

- Social Security Administration — 2026 Annual Report of the Board of Trustees.

- Committee for a Responsible Federal Budget (CRFB) — Analysis of the 2026 Social Security Trustees’ Report.

- Congressional Budget Office (CBO) — Social Security Long-Term Projections.

- Bipartisan Policy Center — 2026 Social Security Trustees Report, Explained.

- Fast Company / Penn Wharton Budget Model — Social Security insolvency projections.

- CBS News — Social Security recipients face looming benefit cuts. Can the program be saved?.

- CRFB — A Six Figure Limit for Social Security.

- Fox Business / “One Big Beautiful Bill Act” references — Social Security has less than 10 years before reserves are exhausted.